More about the interest poster

Interest Rate Chart

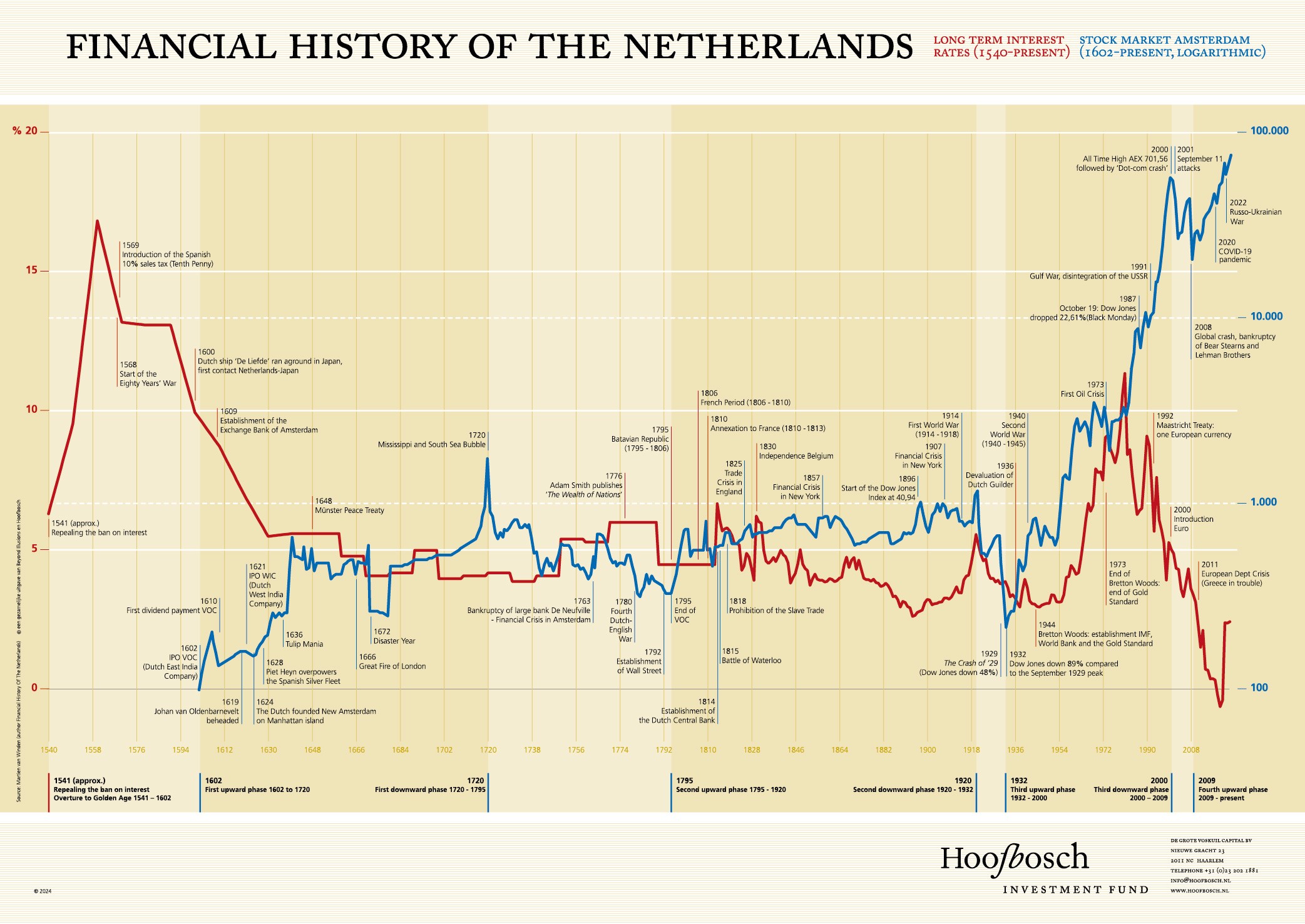

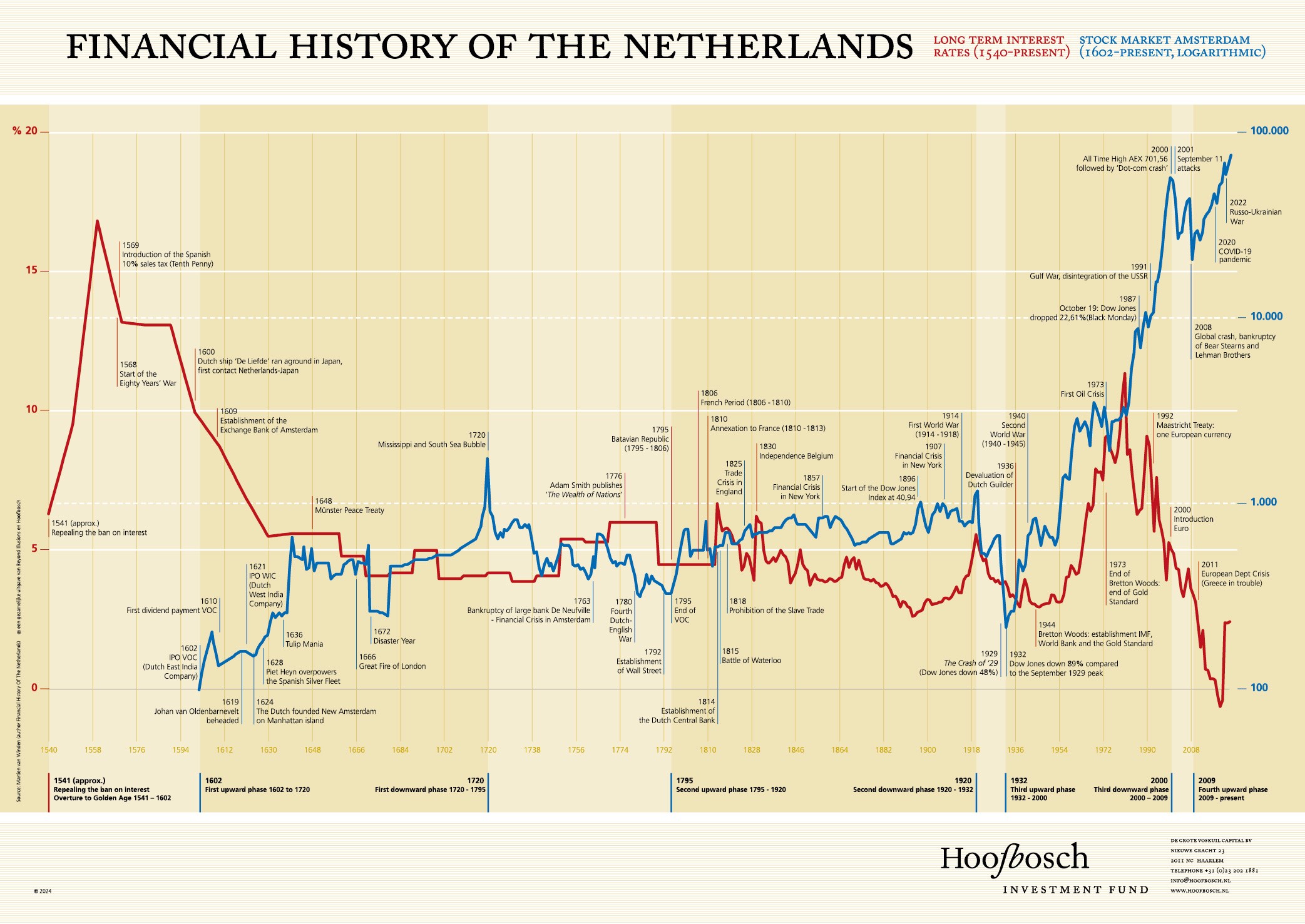

Working with Beyond Illusions, Hoofbosch Investment Fund has created an historical graphic overview of Dutch stock prices and Dutch interest rates in poster form. It captures Dutch interest rates starting in 1541 and stock prices starting in 1601 through end 2024.

{kind=link}

Download the chart here

Books

Je leeftijd als goudmijn

2020 - Voor jongeren die intelligent en nieuwsgierig zijn, maar niet weten hoe de aandelenmarkt werkt en hoe ze ervan kunnen profiteren

Wereld op een keerpunt

2018 — Een blik op de hedendaagse politieke, economische en sociale uitdagingen — Robbert-Jan Engels als mede-auteur

De financiële canon van Nederland

2010 - Lessen uit het verleden zijn een garantie voor de toekomst

Slag om de toekomst

2003 — Een studie over scenarioplanning

Nederland, de schatkist van Europa

2002 - Analyse van de gevolgen van de invoering van de euro voor de welvaart in Nederland

Rijk Blijven

2000 — Over de Nederlandse economische geschiedenis